Momentum CFO is proud to announce that its Founder and President, Rosemary Linden, has been named 2025 CFO of the Year in the Consulting CFO category by the San Diego Business Journal. The award honors outstanding chief financial officers whose strategic foresight, financial acumen, and leadership have driven company growth, shaped organizational success, and made a positive impact on the San Diego community.

“I’m honored to be named CFO of the Year by the San Diego Business Journal. This recognition is especially meaningful because it reflects the mission of Momentum CFO: helping growing businesses access the same caliber of financial expertise that larger corporations rely on. Smaller businesses deserve that level of financial clarity and strategy — and I’m proud to play a part in making it possible, Linden said. “It also validates the leap I took in founding Momentum CFO in 2016, when consulting CFOs were uncommon. Most importantly, I’m incredibly grateful for the trust my clients place in me and remain committed to delivering excellence in every engagement,” Linden said.

Strategic Financial Leadership for Growing Businesses

Linden began her career in Arthur Andersen’s Strategy, Finance, and Economics consulting practice, an early foundation that blended financial expertise with strategic problem-solving. Over the course of her 25+ year career, including the past nine leading Momentum CFO, she has built a diverse background spanning Fortune 500 corporations, founder-led startups, and nonprofit organizations. She has guided finance teams at companies such as WD-40 Company and Quest Diagnostics, managing complex budgets and supporting executive teams across industries including professional services, healthcare, technology, and consumer products.

Today, through Momentum CFO, she brings enterprise-level experience to midsize companies that are scaling but not yet ready for a full-time finance executive. Her consulting work gives leaders the financial visibility they need to make informed decisions. Accounting shows what happened; finance helps anticipate what comes next. By applying this forward-looking lens, Linden helps businesses plan for expansion, allocate resources effectively, and make strategic decisions in uncertain economic conditions.

Delivering Insight and Impact for Business Leaders

Linden’s recognition as CFO of the Year underscores how she equips organizations with the financial discipline and strategic insight they need to scale profitably and sustainably. She has helped clients design profitable pricing strategies, develop long-term forecasts, and implement executive dashboards that connect leadership decisions to business performance. She works closely with executives, investors, and boards to ensure they have clear, decision-ready insights to guide growth.

A central part of her approach is helping companies establish Financial Planning & Analysis (FP&A) capabilities that turn financial data into forward-looking guidance and position finance teams as true partners in business strategy. “My role is not simply to deliver numbers, but to build the financial infrastructure that supports growth and empowers leaders to act quickly and decisively,” Linden said.

Leadership and Mentorship

Beyond her client work, Linden contributes to the profession as a member of the Association for Financial Professionals’ North American FP&A Advisory Council, a national body that shapes standards, certifications, and best practices for corporate finance. She also serves on the leadership team of San Diego Women in Finance, supporting initiatives that connect and elevate women in the field. Mentorship is central to her approach. “One of the most rewarding aspects of my career has been encouraging women to see themselves in leadership roles, including becoming CFO,” she noted.

What Being Named CFO of the Year Means

Being named CFO of the Year is both a milestone and a motivator. “Companies need strong financial leadership to navigate challenges, from growth to changing economic conditions,” she said. “Momentum CFO exists to provide that leadership, and this award strengthens my commitment to the San Diego business community and beyond.”

The recognition reflects Linden’s ability to combine technical expertise with strategic insight, delivering stronger financial results and greater confidence to executives, boards, and investors.

https://momentumcfo.com/wp-content/uploads/2025/09/Rosemary-Linden-2025-CFO-of-the-Year-2.png8001200Momentum CFOhttps://momentumcfo.com/wp-content/uploads/2022/01/momentum-cfo_brand-identity_Final_RGB_Signature_Full-Color-1030x254.pngMomentum CFO2025-09-08 10:45:222025-09-08 10:55:53Rosemary Linden Named 2025 CFO of the Year by San Diego Business Journal

A price isn’t just a number on an invoice. It’s one of the most powerful levers that can impact your business’s profitability and growth. With the right pricing strategies for growing businesses, you can cover costs, safeguard profit margins, and set your company up for long-term success.

For many leaders, though, pricing decisions feel uncertain. Set prices too high, and you risk losing customers. Set them too low, and profit margins shrink until your business can’t sustain itself.

That’s why choosing the right approach matters. In this guide, we’ll explore the most effective business pricing methods, show you how to evaluate which ones are best for your company, and explain how financial analysis provides the insight to make pricing a strategic advantage.

Why Pricing Matters for Growing Businesses

Pricing decisions impact more than revenue. They set the foundation for your company’s profitability and growth trajectory. For growing businesses, the right approach to pricing can mean the difference between steady expansion and stalled momentum.

Effective business pricing strategies help you:

Protect profit margins. A clear strategy ensures you cover costs and earn sustainable returns, even when costs increase.

Position your business in the market. Pricing communicates whether you’re a budget option, a mid-market competitor, or a premium brand.

Support long-term growth. Thoughtful pricing balances short-term revenue goals with building customer loyalty and market share.

Strengthen decision-making. A clearly defined pricing framework reduces guesswork and inconsistency, particularly as your business scales.

Weak pricing practices can quietly erode profitability over time. This often happens when businesses set prices without analyzing costs, copy competitors’ pricing, or neglect to review pricing as circumstances change.

Business Pricing Methods Explained

What’s the best pricing strategy for your business? There is no one-size-fits-all solution. There are many different business pricing methods. Each method has strengths, limitations, and ideal use cases. The most effective strategy often blends several approaches to balance profitability, competitiveness, and customer value.

Common business pricing methods include:

Cost-Plus Pricing

This straightforward method starts with your costs and adds a markup to ensure profit. It’s simple to calculate and ensures you cover expenses, but it doesn’t account for what customers are actually willing to pay.

Value-Based Pricing

With value-based pricing, you set prices according to the customer’s perceived value rather than the cost to deliver. This can support higher margins and brand positioning but requires deep knowledge of your customers and market.

Competitive Pricing Strategy

Here, prices are based on what competitors charge. It helps you stay in line with the market, but this method is reactive rather than proactive. You must constantly monitor changes in your competitors’ pricing.

Penetration Pricing

With penetration pricing, you set a low initial price to quickly win market share. It can work for new products or services but makes it harder to raise prices later without losing customers.

Premium Pricing

Premium pricing positions your offering as high value by charging more than competitors. This strategy can be very profitable, but requires a strong brand and customers who are willing to pay for exclusivity.

Tiered or Freemium Models

Common in SaaS and subscription businesses, these models let customers choose from different levels of service or features. They can drive growth and retention but need careful analysis to avoid underpricing higher tiers.

Psychological Pricing

This method uses behavioral tactics such as charm pricing ($9.99 is more appealing than $10), bundling, or anchoring higher-priced options to make other tiers look more attractive. It can influence buying decisions but must be used thoughtfully to maintain trust.

Factors That Influence Your Business Pricing Strategy

Even the most well designed pricing strategies for your growing business won’t succeed if you ignore the forces that shape customer demand and cost structure. To make confident pricing decisions, you need to account for both internal and external factors, including:

Business Goals

Pricing should support your business objectives. For example, if growth is the priority, you may accept slimmer margins in the short term. If profitability is the focus, you’ll need strong guardrails around discounting practices.

Cost Structure

It’s crucial to understand the total costs of producting your products and services, including expenses such as direct materials, labor, and overhead. Your business’s prices must exceed the costs of production in order to protect profit margins.

Customer Value

The price customers are willing to pay often depends on their perceived value of your products and services. This includes product quality, brand reputation, service levels, and how well your solution solves their problems.

Competitive Landscape

Your competitors influence customer expectations as well. Benchmarking competitors’ prices is important, but relying solely on their pricing risks undercutting your value.

The Impact of Tariffs on Profitability

Inflation, supply chain volatility, and tariffs can quickly impact your financial results. A sudden increase in import costs, for example, will erode margins if prices remain unchanged. Monitoring these pricing pressures and planning how to respond is essential for protecting profitability and sustaining growth.

The Role of Financial Analysis in Pricing

Choosing the right business pricing method is only part of the equation. To understand how pricing decisions truly affect your company, you need financial analysis. This is what connects pricing to profitability.

Financial analysis helps you:

Model different scenarios. What happens to profit margins if prices increase by 5%? What if tariffs raise material costs by 10%? Modeling these scenarios shows the financial impact before you implement changes.

Measure profitability in detail. Looking only at total profitability isn’t enough. Strong overall results can mask that margins may be too low for specific products, services, or customers. Measuring profitability at a more granular level provides the visibility you need to identify what’s truly driving returns.

Track performance over time. Reports, dashboards, and KPIs reveal how actual results compare to the assumptions you made when setting prices. If revenue or profit margins decrease, it’s time to reassess the strategy.

Align pricing with business goals. Whether your objective is growth, market share, or higher profitability, financial analysis gives you the insight to price accordingly.

When pricing is backed by data, you can move from guesswork to confident decision making. That shift is what transforms pricing from a short-term tactic into a long-term advantage.

Common Pitfalls in Business Pricing Methods

Even the best pricing strategy won’t work if it isn’t applied consistently. Many growing businesses fall into predictable traps that limit profitability and growth. Be sure to avoid these common pitfalls.

Setting prices without detailed cost analysis

If you don’t understand your total costs, you risk underpricing your products and services and failing to generate sustainable margins.

Copying competitors’ pricing

Benchmarking is useful, but pricing solely in reaction to competitors puts pricing strategy in their hands instead of yours.

Neglecting regular pricing reviews

Pricing shouldn’t be set once and forgotten. Scheduling routine reviews provides the opportunity to reassses and revise your approach as circumstances change. This protects profitability and ensures your strategy remains aligned with business goals.

Overcomplicating pricing

Complex models and too many pricing tiers can confuse customers and your sales team, making it harder to communicate value and close deals. Keep it simple.

Building a Pricing Playbook

A pricing playbook provides a consistent framework for your team to follow. It documents how your business approaches pricing, who is responsible, and how often strategies are reviewed. For growing companies, a playbook provides the discipline needed to protect profit margins as you scale.

Define your objectives

Clarify what pricing should achieve. Common objectives are increasing profitability, revenue, or market share, or strengthening brand awareness. Connecting these objectives to your company’s broader goals ensures consistency.

Set guiding principles

Establish the rules of the road. For example, define minimum profitability thresholds, how discounts are approved, and whether your business positions itself as premium, competitive, or value-oriented.

Choose your business pricing method

Document which method you’ll use and when. For instance, you may begin with a competitive approach for new offerings and transition to value-based pricing as you learn more about your customers.

Create tools and templates

Develop calculators, margin sensitivity models, and pricing approval checklists. These tools give decision-makers clear, repeatable processes instead of relying on guesswork.

Assign roles and responsibilities

Identify who owns pricing decisions, who monitors market changes, and when leadership approval is required. Clear accountability reduces inconsistency.

Review and adjust regularly

It’s important to review your business’s pricing regularly. Use reports and dashboards to track profitability and customer feedback to inform pricing decisions.

Key Takeaways

Pricing is one of the strongest levers for profitability and growth.

The right business pricing strategies and methods depend on your costs, customers, competitors, and overall goals.

External factors such as tariffs and inflation can quickly impact profitability if prices aren’t adjusted.

Financial analysis helps you test scenarios, measure detailed profitability, and track results over time.

Common pitfalls include skipping cost analysis, copying competitors, neglecting reviews, and overcomplicating models.

A pricing playbook creates consistency by defining objectives, setting principles, assigning responsibilities, and encouraging regular performance reviews.

The Bottom Line

Choosing the right business pricing method isn’t about chasing competitors or reacting to short-term pressures. It’s about using a strategy backed by financial analysis to ensure that your company grows profitably and sustainably.

Your pricing approach should be intentional, documented, and reviewed regularly. With a playbook in place, you can make pricing a strategic advantage rather than a guessing game.

Running a business can feel like riding a roller coaster. Some years, profit comes easily. Other years, unexpected events such as economic downturns or supply chain disruptions can send your results into the red.

If you’re unsure whether the sum of your financial decisions will lead to profit or loss at year-end, it may feel unsettling. The good news is that there are concrete steps you can take to stabilize results and grow consistently. Here are proven strategies to increase profit in your business.

Understand Your Numbers

Profitability is not just about whether you made money; it’s about how efficiently you did it. That’s why you should look beyond total profit, which is the dollar value, and focus on profit margins, which are ratios in your income statement (P&L). Three measures are especially useful:

Gross Margin – Revenue minus the direct cost of producing your product or service. This shows how much money you keep after covering production costs.

Operating Profit Margin – Operating income divided by revenue. This accounts for overhead such as salaries, rent, and marketing, giving you a clearer view of core business performance.

Net Profit Margin – Net income divided by revenue. This is the “bottom line” after all expenses, interest, and taxes.

Tracking these margins over time helps you answer important questions:

Are rising costs eating into profits?

Is overhead in line with revenue growth?

Is the business generating enough return for the risk you are taking?

Regular financial reviews, supported by charts, analysis, and clear explanations, make it easier to spot trends, identify risks early, and take action before problems grow.

Revisit Your Pricing

Your pricing strategy directly affects profitability. If prices are too high, you may lose sales. If they are too low, you are leaving money on the table.

Ask yourself:

Did I base pricing on gut feel or solid market research?

Have I factored in all direct and indirect costs?

Am I achieving an appropriate margin on every sale?

Even small adjustments in pricing can have an outsized effect on your bottom line.

Analyze Product and Service Profitability

Not all revenue contributes equally to your bottom line. Some products or services generate strong margins, while others quietly drain it. Without analysis, it is easy to assume popular offerings are profitable when they may actually be undermining profitability.

Start by reviewing gross margin for each offering and comparing it to the time and resources required to deliver. This often reveals that certain low-volume items are highly profitable, while high-volume ones barely break even.

This insight allows you to refine your mix by adjusting prices or discounts, discontinuing unprofitable items, and doubling down on offerings that truly drive profit.

Manage Expenses Wisely

Strong profit depends not just on revenue, but also on how effectively you manage expenses. Begin by separating non-discretionary expenses such as rent, insurance, and production costs)from discretionary expenses like dues and subscriptions, conferences, and entertainment.

Look for ways to manage both categories more effectively. This could mean renegotiating supplier contracts, automating manual tasks to reduce labor costs, analyzing marketing ROI, or setting clearer guidelines for employee spending.

Thoughtful reductions add up over time and, more importantly, free cash for reinvestment in growth.

Refinance High-Interest Rate Debt

Financing can be essential for growth, but debt at high interest rates can quickly erode profits. If interest expense is eroding profitability, explore refinancing options.

Businesses with consistent profitability are in a stronger position to secure lower-cost financing, which in turn creates more room for reinvestment. If you want to understand how broader economic shifts impact your financing costs, our post on how interest rate changes affect your business explains what rising or falling rates mean for borrowing and long-term profitability.

The Bottom Line

Profit is the foundation of long-term business success, and improving it requires focus on the areas that matter most. When you understand your numbers, refine your pricing, prioritize profitable offerings, manage expenses effectively, and reduce costly debt, you create the conditions for sustainable growth. Stronger profit margins give you flexibility, resilience, and the confidence to make decisions that move your business forward.

Momentum CFO helps business leaders turn financial information into strategies that drive results. If you are ready to strengthen your bottom line, schedule a free consultation today and let’s work together to grow your business profitably.

https://momentumcfo.com/wp-content/uploads/2020/08/Proven-Strategies-to-Increase-Profit.png8001200Momentum CFOhttps://momentumcfo.com/wp-content/uploads/2022/01/momentum-cfo_brand-identity_Final_RGB_Signature_Full-Color-1030x254.pngMomentum CFO2025-08-31 17:03:002025-09-04 09:08:13Proven Strategies to Increase Profit

As a small business owner, you may wonder: Bookkeeper vs accountant vs CFO—what’s the difference? Many business owners use these terms interchangeably, but each has unique responsibilities. Knowing the distinction helps you build the right team for accuracy, compliance, and strategy.

(For a deeper dive into how accounting differs from finance, read our post on Accounting vs. Finance.)

The Role of a Bookkeeper

A bookkeeper is often the first financial professional a small business hires. Their focus is transactional—recording and organizing day-to-day activity in software such as QuickBooks Online.

Common tasks include:

Entering sales, expenses, and payroll transactions

Reconciling bank and credit card accounts

Paying bills and tracking accounts payable

Sending invoices and tracking accounts receivable

Maintaining receipts and financial documents

A good bookkeeper produces monthly reports like the profit and loss statement, balance sheet, and statement of cash flows.

What bookkeepers don’t do: analysis, forecasting, or decision-making. Their role is to keep your records accurate, not to advise on how to improve results.

The Role of an Accountant

An accountant goes beyond bookkeeping. Accountants typically have formal training and are responsible for ensuring financial records are accurate, properly adjusted, and compliant with accounting standards.

Helping business owners interpret results at a basic level

Think of accountants as the bridge between bookkeepers and CFOs. They clean up the data, close the books, and ensure the numbers are reliable. But they typically don’t provide long-term strategy or forward-looking projections.

What About CPAs?

A CPA (Certified Public Accountant) is a licensed accountant who has passed rigorous exams and met state licensing requirements. All CPAs are accountants, but not all accountants are CPAs.

CPAs often focus on:

Preparing and filing taxes

Ensuring compliance with tax laws

Auditing financial statements

Advising on tax strategies

Representing clients in front of the IRS

A CPA is essential for tax planning and compliance. But remember: a CPA often looks backward to ensure taxes and records are correct. A CFO looks forward to shape your overall financial strategy.

The Role of a CFO

A Chief Financial Officer (CFO) is the most strategic member of your financial team. Unlike bookkeepers and accountants, a CFO isn’t just tracking or reporting numbers, they’re helping you make financial decisions that drive growth.

Key CFO responsibilities include:

Measuring financial performance and identifying opportunities to improve profit

Managing cash flow and capital needs

Evaluating risks and financial health

Supporting major decisions like acquisitions or expansions

Partnering with the Board of Directors, providing them with timely, accurate, and meaningful financial information

Advising on fundraising, bank financing, or investor relations

Preparing budgets, forecasts, and strategic plans

Hiring a full-time CFO can be costly for small businesses. That’s why fractional CFO services are a smart option. At Momentum CFO, we provide outsourced CFO expertise so you gain strategic financial guidance without the expense of a full-time executive.

How These Roles Work Together

Here’s how the progression usually looks:

Bookkeeper → gets the numbers into the system.

Accountant → ensures accuracy and compliance.

CPA → handles taxes and audits.

CFO → uses financial insights to shape strategy and guide growth.

Understanding the roles of a bookkeeper vs accountant vs CFO helps you see how each person supports your business at different stages. Each role is distinct, but together they form a complete financial team. Expecting one person to do it all is a common mistake.

The Bottom Line

A bookkeeper, accountant, CPA, and CFO all have critical but different responsibilities. Bookkeepers record transactions, accountants refine them, CPAs handle taxes and audits, and CFOs provide forward-looking strategy.

If you want to strengthen your financial foundation, start by building the right team—and know where each role fits. At Momentum CFO, we help business owners coordinate among financial professionals and provide the strategic guidance that drives profitability.

Ready to add CFO expertise to your team? Book a free consultation and let’s explore how outsourced CFO services can support your growth.

https://momentumcfo.com/wp-content/uploads/2020/04/What-are-the-key-Difference-between-a-bookkeeper-CFO-CPA-Thumb.jpg9231500Momentum CFOhttps://momentumcfo.com/wp-content/uploads/2022/01/momentum-cfo_brand-identity_Final_RGB_Signature_Full-Color-1030x254.pngMomentum CFO2025-08-30 16:12:002025-09-04 09:17:36Bookkeeper vs. Accountant vs. CFO: Key Roles Explained

If you’ve ever wondered how to read a balance sheet without a strong finance background, this guide is for you. Many executives and business owners focus heavily on the income statement (P&L) while overlooking the balance sheet, even though it provides an important view of your company’s financial position: what the business owns, what it owes, and what belongs to owners.

At Momentum CFO, we work with business leaders to transform financial statements into practical insights. This guide explains how you can use the balance sheet to assess risk, identify growth opportunities, and build a stronger foundation for the future.

What Is a Balance Sheet?

The balance sheet is one of the three core financial statements, along with the income statement and the cash flow statement.

Financial Statement

Time Frame

What it Shows

Balance Sheet

Point in time (e.g., May 31)

Assets, liabilities, equity (financial position)

Income Statement (P&L)

Period (month/quarter/year)

Revenue, expenses, profit or loss (performance)

Cash Flow Statement

Period (month/quarter/year)

Cash inflows/outflows from operating, investing, and financing activities

Unlike those, which measure performance or cash flows over a period of time, the balance sheet is a snapshot of a single point in time.

The balance sheet has three main sections:

Assets – what your company owns and uses to operate.

Liabilities – what your company owes to creditors.

Equity – what remains for owners after liabilities are paid.

Together, these three sections provide a full picture of your company’s financial health.

The Balance Sheet Equation

At the heart of every balance sheet is a simple equation:

Assets = Liabilities + Equity

Or restated:

Equity = Assets – Liabilities

This balance sheet must always balance. Every dollar of assets is financed either by debt (liabilities) or by owners’ investment (equity).

The Three Sections of the Balance Sheet

The balance sheet tells a story of your business in three parts:

Assets (What You Own): These are the resources your business uses to create value, including cash in the bank, receivables from customers, inventory, and investments in property or equipment. Strong assets give your business resilience and flexibility.

Liabilities (What You Owe): These are your financial obligations to lenders, suppliers, employees, and tax authorities. Liabilities can fuel growth, but too much reliance on debt can create risk.

Equity (What Belongs to Owners): This is the value left over for owners after paying off liabilities. Equity reflects how much of the business is truly yours.

When you understand how these sections fit together, you can see whether your company is building value, straining under debt, or balancing the two.

Assets: What You Own

Assets are divided into two categories: current assets (convertible to cash within 12 months) and non-current/long-term assets (held for longer).

Current Assets include:

Cash & Cash Equivalents – Bank balances or short-term investments.

Accounts Receivable (A/R) – Customer invoices not yet collected.

Inventory – Raw materials, work-in-progress, finished goods.

Prepaid Expenses – Payments made in advance (insurance, rent).

Other Current Assets – Deposits, employee advances.

Goodwill – Value recorded when a company buys another business for more than the fair market value of its assets. It reflects things like brand reputation, loyal customers, or strong relationships that add value beyond physical assets.

Why it matters: Monitoring assets shows whether growth is supported by liquid resources like cash or tied up in less flexible forms such as inventory and equipment. This perspective helps you manage liquidity, prioritize investments, and ensure your resources align with your strategy.

Liabilities: What You Owe

Liabilities are also divided into current and non-current categories.

Current Liabilities include:

Accounts Payable (A/P) – Vendor bills not yet paid.

Accrued Expenses – Wages, taxes, utilities incurred but not paid.

Short-Term Debt – Lines of credit, loan installments due within a year.

Deferred Revenue – Payments collected before delivering products/services.

Other Current Liabilities – Sales tax payable, credit cards, short-term leases.

Non-Current Liabilities include:

Long-Term Debt – Bank loans, bonds, or leases due after one year.

Why it matters: Comparing liabilities to assets helps you assess whether your company can comfortably meet obligations or is becoming overleveraged. The right balance of debt supports growth, but too much risk can limit flexibility and make financing more costly.

Equity: What Belongs to Owners

Equity represents the portion of the business that belongs to its owners after all debts are paid. It shows how much of the company’s value is truly yours.

Key components include:

Owner’s or Shareholders’ Equity – The owners’ stake in the business.

Retained Earnings – Profits the company keeps and reinvests instead of distributing to owners.

Paid-In Capital – Money invested directly by owners or shareholders, such as startup funding or later capital raises.

Treasury Stock – Shares a company has repurchased. This reduces total equity because cash was used to buy back ownership.

Why it matters: Tracking equity over time shows whether the business is truly creating value for its owners. Growth fueled by profits reflects a strong, self-sustaining company, while growth that depends mainly on capital infusions can signal underlying weaknesses.

Key Metrics for Business Leaders

You don’t need to memorize formulas, but a few simple ratios can help you quickly gauge financial health:

Working Capital = Current Assets – Current Liabilities Measures liquidity: do you have enough resources to cover obligations?

Current Ratio = Current Assets ÷ Current Liabilities Assesses short-term solvency. Ratios below 1 suggest strain; many businesses target 1.2–2.0 depending on industry.

Debt-to-Equity = Total Liabilities ÷ Equity Shows leverage. High ratios increase risk if profits decline.

Why it matters: These ratios act like dashboard signals for your business. When they shift in the wrong direction, it’s a sign to look deeper and take corrective action before small issues turn into bigger challenges.

What Your Balance Sheet Can Tell You

Once you know how to read a balance sheet, you can use it to:

Gauge liquidity: Can you fund day-to-day operations without stress?

Spot risks: Are receivables piling up or inventory growing faster than sales?

Assess leverage: Is debt fueling smart growth or creating fragility?

Support decisions: From hiring and expansion to preparing for investors, your balance sheet provides critical context.

The Bottom Line

The balance sheet is a leadership tool, not just a financial report. It shows how your company is funded, how effectively resources are being used, and whether long-term value is being created for owners.

When you understand how to read a balance sheet, you can connect the numbers to strategy. You’ll see whether growth is sustainable, whether risks are emerging, and where opportunities lie. This understanding turns financial statements from static reports into tools for confident decision-making.

At Momentum CFO, we help business leaders move beyond the numbers to take decisive action—strengthening cash flow, optimizing capital structure, and building the foundation for future growth.

https://momentumcfo.com/wp-content/uploads/2025/08/Balance-Sheet.png8001200Momentum CFOhttps://momentumcfo.com/wp-content/uploads/2022/01/momentum-cfo_brand-identity_Final_RGB_Signature_Full-Color-1030x254.pngMomentum CFO2025-08-21 10:55:462025-09-01 18:40:30How to Read a Balance Sheet

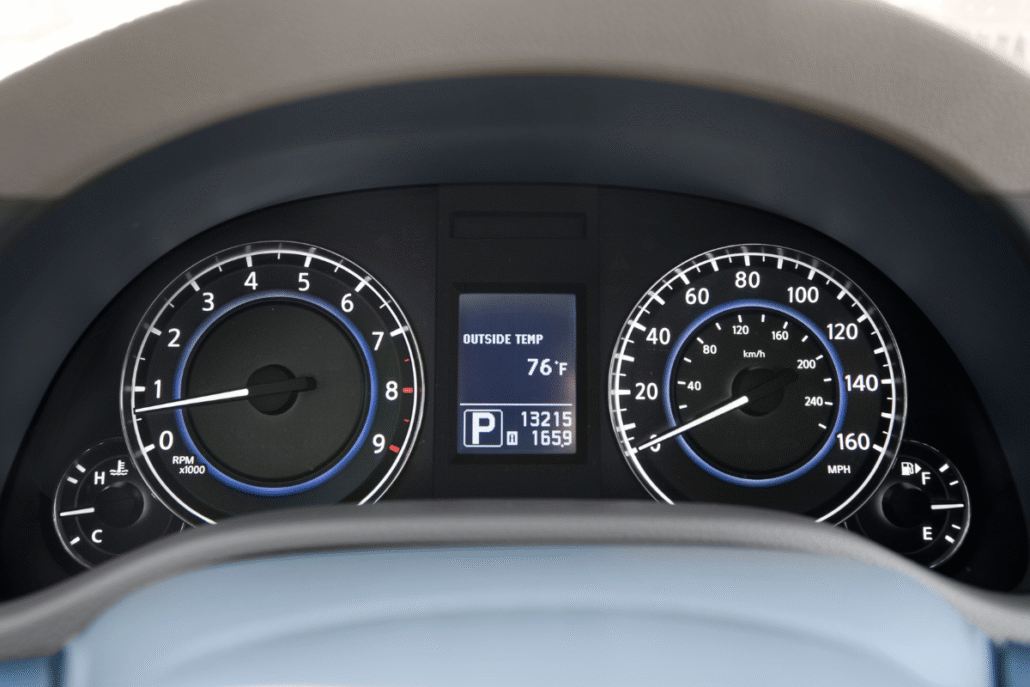

Have you ever wondered about the differences between accounting vs finance? Many business leaders use the terms interchangeably, but accounting and finance are not the same. Knowing the distinction can transform how you run your company.

If your business were a car, accounting would be the gauges on your dashboard — the odometer, fuel gauge, and temperature gauge — that tell you exactly how far you’ve traveled, how much fuel you have left, and the current status of your engine. Finance would be your navigation system, mapping the best route to your destination, helping you adjust when plans change, and ensuring you get there as efficiently as possible.

What is Accounting? (Your Car’s Gauges)

The Corporate Finance Institute (CFI) defines accounting as “the recording, maintaining, and reporting of a company’s financial records.” (CFI)

The Association for Financial Professionals (AFP) adds that “Accounting is focused on the past. They record the transactions, report the information to management and stakeholders, and ensure compliance in their reporting through a standardized set of rules.” (AFP)

In practice, accounting means:

Recording every transaction accurately

Preparing financial statements such as the income statement, balance sheet, and cash flow statement

Ensuring compliance with tax laws and accounting standards

Creating a clear, verifiable record of the company’s financial history

Just like your car’s gauges, accounting provides precise readings of what has already happened and your current status. It doesn’t decide where you’re going — it simply gives you the facts so you can drive safely and legally.

What is Finance? (Your Navigation System)

CFI defines finance as “the management of money and investments for individuals, corporations, and governments.” (CFI)

Finance uses the historical data from accounting to:

Forecast revenue, expenses, and cash flow

Build budgets and long-range plans

Evaluate investment opportunities

Model “what if” scenarios to guide decision-making

The perspective is different too. Accounting typically focuses on the past, while finance focuses on the future.

In the car analogy, the navigation system takes the information from your gauges and uses it to chart the best route to your destination. It can reroute you around traffic, help you decide whether to take the toll road, and anticipate fuel stops before you run low.

This is where Momentum CFO comes in. We focus on the navigation system, helping growing businesses use forward-looking finance to guide strategy. We work alongside your accounting team to turn accurate historical records into forecasts, scenarios, and plans that point your business in the right direction and keep it on course.

Where FP&A Fits In

Financial Planning & Analysis (FP&A) is a specialized area within finance focused on driving strategy and improving decision-making. AFP explains: “FP&A is future-focused. These professionals improve business decisions across the organization by supporting the allocation of capital to its most productive use.” (AFP)

FP&A professionals often:

Build financial models to evaluate different strategic options

Partner with business leaders to create budgets and forecasts

Analyze performance metrics and trends to inform leadership decisions

At Momentum CFO, FP&A is at the core of what we do. Think of it as the advanced navigation system that considers traffic patterns, fuel efficiency, and weather so you can reach your business goals faster, with fewer surprises, and with the confidence that you are taking the best route available.

Key Accounting and Finance Differences at a Glance

Aspect

Accounting

Finance

Time Focus

Past

Future

Primary Goal

Accuracy and compliance

Strategy and decision-making

Responsibilities

Recording transactions, managing accounts receivable and payable, preparing financial statements, auditing financial records, ensuring compliance with regulations

Analytical and quantitative thinking, problem-solving, planning, influencing decisions

Overlap in Smaller Businesses

While larger companies have both accounting and finance staff, in smaller companies, accounting staff such as the Controller, may handle both accounting and some finance tasks. While this can cover basic needs, it often leaves finance in a reactive mode. Without a dedicated navigation system, you risk missing better routes, failing to spot risks early, or making short-term decisions that do not align with long-term goals.

Why the Differences Matter

Understanding the differences between accounting and finance helps you:

Avoid gaps in financial insight

Use the right expertise for the right task

Make better, faster, decisions,

Support growth with both accuracy and strategy

In short, without the gauges you lose track of your status. Without the navigation system you may keep driving in circles.

The Bottom Line

Understanding the difference between accounting vs finance is more than semantics. It’s about ensuring your business has both an accurate record of its past and a clear, strategic plan for its future. Accounting keeps your record straight. Finance charts your course forward. Together, they help you run your business with clarity, confidence, and purpose.

Ready to put a high-performing navigation system in place for your business?Let’s talk!

https://momentumcfo.com/wp-content/uploads/2025/08/Accounting-vs-Finance.png8001200Momentum CFOhttps://momentumcfo.com/wp-content/uploads/2022/01/momentum-cfo_brand-identity_Final_RGB_Signature_Full-Color-1030x254.pngMomentum CFO2025-08-15 13:17:372025-08-21 11:11:35Accounting vs Finance: Understanding the Differences

The types of business budgets your company uses can make the difference between guesswork and clarity when planning for growth. Many leaders picture a single spreadsheet of revenues and expenses, but in reality, budgeting is more structured than that, especially as your company scales.

A master budget isn’t one document. It’s a coordinated framework built from three types of business budgets: the operating budget, the capital expenditure budget, and the cash budget. According to the Corporate Finance Institute, “Understanding the master budget and its components is a critical step in building a budgeting process that aligns strategy with planning and resource allocation.”

When businesses first implement a budgeting process, they usually begin with the operating budget because it ties directly to revenue and expenses. While that’s a natural starting point that illustrates profitability, it’s only part of the picture. The cash budget and capital expenditure budget are equally important for ensuring liquidity and funding future growth.

Operating Budget

The operating budget is the backbone of the master budget. It outlines expected revenues, cost of goods sold (COGS), and operating expenses for a period, usually one year.

Think of it as the company’s day-to-day financial plan. It outlines expected sales, staffing needs, expenses, and the resulting profit or loss.

For growth companies, the operating budget is critical because:

Sales forecasts set the tone. An accurate sales projection drives production, hiring, and marketing spend.

Expense discipline matters. As overhead grows, you need a clear view of costs to protect margins.

Variance analysis improves agility. Comparing actuals to budget shows where you’re overspending or outperforming.

A strong operating budget provides early insight into profitability—whether your model works at scale.

Capital Expenditure Budget

Growth requires investment. New equipment, facilities, or enterprise technology often come with a hefty price tag. That’s where the capital expenditure budget, or CapEx budget, comes in.

The CapEx budget is a business’s plan for long-term investments in fixed assets—property, plant, equipment, and other resources that support the company’s growth. Unlike the operating budget, which covers daily activity, the capital budget focuses on the big-ticket investments that fuel expansion.

As the Association for Financial Professionals explains, “The goal of capital budgeting is to determine whether an investment or project is worth pursuing, and to ensure the company’s capital resources are efficiently allocated.” In practice, this means evaluating not only the financial return on a project, but also whether it aligns with the company’s long-term strategy.

For growing businesses, a CapEx budget is essential because it:

Prioritizes investments. Not every initiative can be funded at once. A disciplined capital budgeting process helps leaders weigh opportunity costs and direct resources toward the investments that matter most.

Supports financing. Large purchases may require debt or equity. Planning ahead helps secure favorable terms.

Prepares for scale. Whether it’s a warehouse, production line, or enterprise software, capital expenditures help prepare the business for expansion and long-term growth.

Without a CapEx budget, companies risk allocating capital to projects that strain cash flow and undermine long-term stability.

Cash Budget

Even profitable companies can run into trouble if they don’t have cash on hand when bills come due. That’s why the cash budget is such an important piece of the master budget.

The cash budget is a plan that details cash inflows and outflows. It captures client payments, payroll, vendor obligations, loan repayments, and other movements of cash.

For growth companies, the cash budget is essential because it:

Highlights liquidity risks. Even profitable businesses can face a cash crunch if customer payments lag or expenses rise unexpectedly. For more on common pitfalls, see our post on cash flow mistakes that can sink your business.

Guides financing. A clear cash budget shows when you’ll need outside funding and helps you time debt or equity raises.

Prevents stalls. With visibility into future cash needs, you can fund hiring, inventory, and marketing without slowing momentum.

A solid cash budget gives leaders the foresight to act before problems emerge.

How the Three Budgets Work Together

Each of the three types of business budgets serves a unique purpose, but they’re interdependent.

The operating budget drives day-to-day profitability.

The capital expenditure budget maps long-term investments.

The cash budget ensures liquidity to execute both.

Together, they provide a full picture of financial health and future needs. They help leaders see not only where the business is heading, but whether resources are in place to get there.

Many growth-stage companies struggle because they rely too heavily on the operating budget alone. By layering in capital and cash budgets, you move from reactive planning to proactive strategy.

For a deeper review of how well your budgeting process supports your goals, consider starting with a Financial Health Check™.

The Bottom Line

Strong budgets don’t just keep the numbers in order. They give you the insight to make faster, better business decisions. By combining operating, capital expenditure, and cash budgets into a master budget, you create the roadmap to scale with confidence.

https://momentumcfo.com/wp-content/uploads/2025/09/1.png8001200Momentum CFOhttps://momentumcfo.com/wp-content/uploads/2022/01/momentum-cfo_brand-identity_Final_RGB_Signature_Full-Color-1030x254.pngMomentum CFO2025-07-24 17:06:002025-09-24 17:10:04Types of Business Budgets: Three Parts of a Master Budget

Budgeting isn’t just about plugging numbers into a spreadsheet. The business budgeting methods you use shape how your leadership team thinks about spending, accountability, and strategy. For midsize businesses, choosing the right approach can be the difference between running on autopilot and building a financial roadmap that supports growth.

In a recent post, we explained the three core types of business budgets — operating, capital expenditure, and cash — and how each plays a role in financial planning. This article builds on that foundation by looking at how budgets are constructed. We’ll explore four common business budgeting methods: incremental, zero-based, activity-based, and value proposition. For each, we’ll cover the definition, an example, pros and cons, and when it’s most useful.

Incremental Budgeting

Incremental budgeting takes last year’s budget as a starting point and applies modest adjustments, often a flat percentage increase or decrease. The assumption is that past spending patterns are a reasonable baseline for the year ahead.

Consider a company that spent $250,000 on software licenses last year. With headcount expected to rise by 10%, the IT budget might simply be lifted by the same percentage to cover additional licenses and support. No deeper analysis is done . The increase is simply layered on top of last year’s spend.

Pros and Cons of Incremental Budgeting

The appeal of incremental budgeting is its simplicity. It’s quick to prepare, easy for department leaders to understand, and predictable from year to year. That makes it especially useful for organizations in stable industries where costs and revenues don’t fluctuate dramatically.

But the very simplicity of incremental budgeting is also its biggest weakness. Because it assumes that past spending patterns are appropriate, it tends to carry inefficiencies forward. If last year’s IT budget included underutilized software, those costs roll right into the next cycle without question. The method can also encourage “use it or lose it” behavior, where managers rush to spend their full allocation so it isn’t cut in the next round. Over time, this often leads to “budget creep” — small annual increases that compound into a bloated cost structure.

When to Use Incremental Budgeting

For that reason, incremental budgeting works best for steady, mature businesses with predictable costs. It’s not as effective in volatile industries or for companies that need a sharper lens on expenses. If your company is experiencing growth and change, relying too heavily on incremental adjustments could leave you blind to opportunities for efficiency.

Zero-Based Budgeting

Zero-based budgeting (ZBB) takes the opposite approach of incremental budgeting. Instead of assuming last year’s budget is a good starting point, every line item must be justified from scratch. Leaders begin with a blank slate — or “zero base” — and build their budget by proving the need for each expense.

Imagine a company that historically spends $500,000 on digital marketing campaigns. Under zero-based budgeting, that budget doesn’t simply carry forward. The marketing team must make the case for every campaign, showing the expected ROI and strategic alignment. If a certain channel or event can’t demonstrate value, the expense may be cut entirely.

Pros and Cons of Zero-Based Budgeting

The advantage of ZBB is that it forces accountability. Every dollar is scrutinized, which helps eliminate waste and redirect funds to the highest-value initiatives. It also ensures that resources are aligned with strategy rather than inertia. This can be especially powerful for companies undergoing a turnaround, experiencing margin pressure, or seeking to reset spending habits across the organization.

However, the discipline of zero-based budgeting comes at a cost. Building a budget from scratch requires significant time and resources, particularly for larger organizations with many departments. If applied too rigidly or too often, the process can also create disruption, frustrate managers, and lead to short-term thinking at the expense of long-term investments.

When to Use Zero-Based Budgeting

For these reasons, zero-based budgeting is best used selectively. It works well when companies need to tighten their belts, reset spending priorities, or shine a spotlight on discretionary costs like marketing, travel, or entertainment. But it is rarely practical to apply across the entire organization every year. Many leaders instead use a hybrid approach like applying ZBB to specific categories while using other methods elsewhere.

Activity-Based Budgeting

Activity-based budgeting (ABB) builds the budget around the activities required to deliver products or services, rather than simply rolling forward last year’s numbers. The focus is on understanding cost drivers — the resources each activity consumes — and planning expenses accordingly.

For example, consider a manufacturer that expects to produce 50,000 units of a product next year. Each unit requires a set amount of raw materials, machine time, and labor hours. Instead of taking last year’s production costs and adding a percentage increase, ABB estimates the budget based on forecasted activity levels: 50,000 units × cost of materials per unit, plus the associated machine and labor costs. The result is a budget that directly reflects workload and demand.

Pros and Cons of Activity-Based Budgeting

The strength of ABB lies in its ability to make costs more transparent. By linking expenses to activities, leaders gain a clearer view of what drives their budgets and how changes in demand will affect costs. This makes ABB particularly valuable for organizations with operational complexity, where traditional budgets can hide inefficiencies. It also helps leaders model how scaling up (or down) impacts resource requirements.

On the other hand, activity-based budgeting requires detailed operational data and the ability to measure activities accurately. For smaller businesses without strong systems or cost-tracking capabilities, it can be burdensome to implement. Even in larger organizations, the process adds complexity that some leaders may resist.

When to Use Activity-Based Budgeting

Because of this, activity-based budgeting is best suited for companies where activities can be clearly defined and measured such as manufacturing, healthcare, logistics, or professional services. In these environments, ABB provides a disciplined way to connect financial planning with the real work of delivering products and services.

Value Proposition Budgeting

Value proposition budgeting asks a deceptively simple question: Does this expense create value for our customers or our business? Instead of assuming costs are necessary because they’ve always been there, this method challenges leaders to connect spending directly to value delivered.

Consider a company planning its annual marketing calendar. In past years, it has allocated $200,000 to attend a major trade show. Under a value proposition approach, that line item doesn’t roll forward automatically. The leadership team asks: Does this event generate enough qualified leads, strengthen customer relationships, or enhance our reputation in a way that justifies the cost? If the answer is yes, the expense stays. If not, the funds may be redirected to support initiatives with clearer and more measurable ROI.

Pros and Cons of Value Proposition Budgeting

The strength of value proposition budgeting is that it keeps spending aligned with strategy. By forcing leaders to evaluate how each expense contributes to customer value or business priorities, it reduces waste and helps direct resources toward the highest-impact initiatives. This can build a more disciplined, ROI-focused culture across the organization.

But the method also has its challenges. Value can be subjective, and leaders may disagree on what qualifies. For example, compliance costs or IT infrastructure may not appear to deliver direct customer value, but they are essential to keeping the business running. Without clear criteria, the process risks underfunding critical but indirect functions.

When to Use Value Proposition Budgeting

For this reason, value proposition budgeting works best for growth-focused businesses that want to maximize ROI and ensure their resources are supporting strategic priorities. It is particularly powerful when evaluating discretionary spending like marketing, R&D projects, or new initiatives. The method encourages leaders to look beyond what’s been done in the past and ask, Is this expense truly creating value?

The Bottom Line

The budgeting method you choose shapes more than your financial plan. It influences how your leaders think about costs, priorities, and strategy. Incremental budgeting offers simplicity, zero-based brings discipline, activity-based highlights cost drivers, and value proposition keeps the focus on ROI. Each method has strengths and trade-offs, and the right choice depends on your company’s circumstances.

For many midsize businesses, a hybrid approach works best. Apply incremental budgeting where stability is the goal, use zero-based or value proposition techniques for discretionary categories, and leverage activity-based budgeting where operational complexity demands clarity.

Budgeting is one of the most important planning processes you’ll undertake each year. If you’re wondering whether your current approach is helping your business move forward, it may be time to revisit not just your numbers but the method behind them. Schedule a free introductory consultation with Momentum CFO.

https://momentumcfo.com/wp-content/uploads/2025/09/4-Business-Budgeting-Methods.png8001200Momentum CFOhttps://momentumcfo.com/wp-content/uploads/2022/01/momentum-cfo_brand-identity_Final_RGB_Signature_Full-Color-1030x254.pngMomentum CFO2025-06-30 17:10:002025-09-30 17:11:234 Business Budgeting Methods Explained

Interest rates influence nearly every part of your business—from the cost of financing to customer spending power. Whether rates are rising or falling, understanding their impact helps you make smarter financial decisions and protect your business’s bottom line.

The Federal Reserve sets the federal funds rate, which is the rate at which banks lend to each other overnight. This benchmark affects borrowing costs across the economy. When the Fed adjusts rates, it’s typically in response to economic conditions. The Fed raises rates to cool inflation and lowers them to stimulate growth. You can follow current policy decisions directly on the Federal Reserve’s website.

When Higher Rates Work in Your Favor

Rising rates aren’t all bad news. Banks often increase the interest paid on deposits, which means the cash you keep in reserve may finally generate a meaningful return. If you maintain a strong balance, those extra earnings can add up to thousands of dollars a year. Curious about current rates? Momentum CFO recommends checking Bankrate.com to find the highest rates.

Higher rates can also strengthen the U.S. dollar. When interest rates rise, U.S. assets such as Treasurys often become more attractive to global investors seeking high yields. Increased demand for U.S. assets increases the value of the dollar relative to other currencies. For businesses, a stronger dollar can have clear advantages. If you pay international suppliers or contractors, your purchasing power improves because each dollar buys more of the foreign currency that it did before.

And perhaps most importantly, raising rates is the Fed’s primary tool for controlling inflation. Higher rates make borrowing more expensive, which decreases consumer and business spending. With less demand in the economy, prices stop rising as quickly and inflation eases. A more stable pricing environment reduces uncertainty and helps you plan more confidently.

Challenges of a Rising Rate Environment

Of course, rising rates can make growth more difficult. If you use a variable-rate line of credit or loan, your monthly payments may climb significantly, harming cash flow. Banks also tend to be more selective about approving new credit, which can limit access to financing just when you need it. If you rely on a line of credit, consult Momentum CFO for assistance. We carefully monitor interest rates and will help you mitigate the financial impact of increased interest expense.

On the revenue side, higher household borrowing costs on debt such as mortgages, auto loans, and credit cards leave consumers with less disposable income. That often results in cutting back on discretionary purchases such as dining out, travel, or nonessential products and services. For businesses, weaker demand can quickly translate into lower revenue. In addition, rising interest expense reduces profitability. These pressures can squeeze margins and force difficult decisions about whether to raise prices, delay investments, or reduce costs elsewhere in the business.

Opportunities in a Low-Rate Economy

When the Fed lowers rates, financing becomes more affordable. This creates opportunities to refinance existing loans at lower rates, freeing up cash for growth initiatives like expanding your team, investing in technology, or entering new markets. Lower borrowing costs make it easier to launch new projects or finance acquisitions at a reduced cost of capital.

In addition, banks often ease lending requirements in a low-rate environment. For growing businesses, this can mean higher credit limits, faster approvals, or better loan terms that may not have been available when rates were higher. With more access to capital, you can fund expansion plans that accelerate growth and strengthen your competitive position.

Lower rates can also stimulate consumer spending. With reduced debt service costs, households have more disposable income, which can translate into stronger demand for your business’s products or services.

Tradeoffs of Lower Borrowing Costs

Low rates aren’t without drawbacks. Cash reserves may generate little to no interest, reducing the passive income your business earns from savings. A weaker dollar can also increase the cost of imports, eating into your margins if your supply chain depends on foreign imports. And when borrowing is cheap, demand can overheat, fueling inflation and introducing new cost pressures.

How to Stay Ahead of Rate Changes

No matter which way rates are moving, preparation is the key to staying ahead of the game. The best way to prepare for changing interest rates is with scenario analysis. At Momentum CFO, we conduct scenario analysis to model the financial impact of different rate environments before they affect your business.

Here’s how we approach it:

We build custom financial models that reflect your unique revenue streams, cost structure, and financing mix.

We test multiple scenarios—for example, what happens to your cash flow if interest rates rise by 2%, stay elevated for several quarters, or decrease?

We quantify the impact on borrowing costs, profitability, and liquidity so you can clearly see the risks and opportunities.

We guide your decisions by showing which strategies, such as refinancing, shifting your debt mix, or adjusting pricing, position you best under each scenario.

Instead of guessing how interest rate changes might affect your business, scenario analysis gives you clear, data-driven answers. Uncertainty becomes actionable insight, helping you make confident choices about financing, growth, and investments.

To stay informed about when rates may shift, we also track FOMC (Federal Open Market Committee) statements, and incorporate the Fed’s economic outlook into your business’s planning processes.

The Bottom Line

Interest rates changes cut both ways. They can reward your business with stronger savings and consumer demand, or challenge it with higher borrowing costs and tighter margins. What matters most is how you prepare and respond.

At Momentum CFO, we help business leaders understand financial risks and opportunities tied to changing rates. With decades of financial experience, we build models, forecasts, and strategies that give you confidence in every rate environment.

Ready to see how interest rates affect your business? Momentum CFO can help. Schedule a free consultation to learn how we can help you navigate interest rate changes.

https://momentumcfo.com/wp-content/uploads/2023/03/High-Low-Cover-1200-x-800.png8001200Momentum CFOhttps://momentumcfo.com/wp-content/uploads/2022/01/momentum-cfo_brand-identity_Final_RGB_Signature_Full-Color-1030x254.pngMomentum CFO2024-10-19 18:58:002025-08-22 12:12:38How Interest Rates Impact Your Business

“Entrepreneurs believe that profit is what matters most… But profit is secondary. Cash flow matters most.”

– Peter Drucker

“Entrepreneurs believe that profit is what matters most… But profit is secondary. Cash flow matters most.” – Peter Drucker

Cash is the foundation of your business. It supports every decision, from hiring employees and purchasing supplies to paying debt and investing in growth. Yet many companies overlook cash flow until it becomes a problem. According to the Federal Reserve’s 2024 Small Business Credit Survey, 51% of businesses cite uneven cash flows as challenges. The good news: with the right discipline, you can avoid common mistakes that put your company at risk.

Here are six of the most common cash flow mistakes — and how to prevent them.

1. Overestimating Sales

It’s natural to be optimistic when planning for the future, but relying on overly aggressive sales projections can quickly leave you short on cash. If your budget assumes that every potential deal will close on time, you may not have enough liquidity to cover expenses when sales fall short.

Build both best-case and conservative scenarios. In your conservative model, identify expenses you could scale back, delay, or eliminate if revenue doesn’t meet expectations. Scenario planning gives you a clear plan of action rather than leaving you scrambling if sales underperform. A strong business budget can help provide that framework.

2. Overdue Customer Invoices

A sale isn’t complete until cash is collected. Overdue invoices tie up working capital and make it difficult to cover payroll and other obligations.

Review your accounts receivable aging report every month. Follow up promptly on late payments, and include clear consequences for late payers such as monthly finance charges in your contracts. Consistent enforcement is key; if customers learn there are no consequences for delaying payment, you’ll always be at the bottom of their priority list.

3. Mismatched Payment Terms

When your vendors require payment in 15 days but your customers take 45 days to pay you, the 30-day gap has to be funded by your own cash. If this mismatch continues, it creates chronic cash shortages.

Look for opportunities to renegotiate terms with both vendors and customers. If renegotiation isn’t possible, consider offering small early-payment discounts to customers as an incentive. For ongoing gaps, financing tools like invoice factoring may help, but always evaluate the fees carefully to ensure they don’t erode your margins.

4. Operating Without a Cash Flow Forecast

A bank account balance only shows today’s position. Without forward visibility, you risk being caught off guard by upcoming deficits.

A rolling cash flow forecast projects future inflows and outflows, giving you time to plan. With this visibility, you can anticipate when you’ll need additional cash, adjust spending, or arrange financing in advance. Forecasting also gives you confidence to make growth decisions, such as hiring or investing in new equipment, knowing the impact on liquidity.

5. Failing to Prepare a Backup Plan

Even with strong forecasting, surprises happen: a key customer delays payment, supply costs rise, or economic conditions shift. That’s why a financial safety net is essential.

Aim to keep at least three months of operating expenses in reserve, set aside in a liquid, low-risk account. In addition, establish a line of credit while your financials are strong, not when you’re already under pressure. Access to emergency funds provides flexibility and peace of mind when unexpected challenges arise.

6. Not Knowing Your Numbers

You can’t manage what you don’t measure. Many business leaders focus on generating revenue but don’t dedicate time to financial management. The result: limited visibility into risks and missed opportunities to correct course.

At minimum, review your monthly cash flow statement and profit and loss statement. Together, these reports show where cash is coming from, where it’s going, and whether operations are sustainable. Go a step further by tracking key performance indicators (KPIs) such as days sales outstanding, operating cash flow, and gross margin. These insights highlight risks early, giving you time to act before a crisis develops.

The Bottom Line

Healthy cash flow doesn’t happen by accident. It requires forecasting, disciplined collections, careful management of payment terms, and a solid backup plan. By avoiding these six mistakes, you’ll protect your company from unnecessary surprises and position it for sustainable growth.

For additional ideas on strengthening your finances, explore these five essential financial tips. And if you’d like expert guidance in building cash flow discipline into your business, consider working with a seasoned financial partner. An experienced CFO can help you design forecasts, improve collections, and ensure you always know where your business stands financially. To learn more, schedule your free financial consultation.

https://momentumcfo.com/wp-content/uploads/2020/04/Coping-With-the-Coronavirus-Cash-Flow-Crunch-Thumb.png6281200Momentum CFOhttps://momentumcfo.com/wp-content/uploads/2022/01/momentum-cfo_brand-identity_Final_RGB_Signature_Full-Color-1030x254.pngMomentum CFO2024-08-21 16:20:002025-08-23 10:11:376 Cash Flow Mistakes That Can Sink Your Business

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.

{kind=link}