What Is FP&A?

Many business leaders review financial reports regularly but find it harder to interpret what those numbers mean for the future. Last quarter’s results are clear. What should happen next is less so. This is the gap that financial planning and analysis, or FP&A, is designed to close.

FP&A is a corporate finance function responsible for helping business leaders make better decisions. Accounting records performance. FP&A predicts it. Through planning, forecasting, performance management, and analysis, it gives leadership a forward-looking view of business performance and the financial clarity to act on it.

For growing businesses, that forward view becomes increasingly critical. Growth creates complexity: more customers, more people, more departments, and more financial variables to manage. FP&A provides the visibility to understand what is driving results, where the business is on track or off, and where resources should go next.

Most businesses first encounter FP&A through familiar deliverables: the annual budget, monthly or quarterly forecast updates, variance analysis, KPI reporting, board and investor reporting, and financial models used to evaluate hiring, pricing, investment, or expansion decisions. These are the visible outputs of a function whose real purpose is enabling informed decisions about resources, risk, and growth.

What FP&A Actually Does

FP&A encompasses four core activities: planning, forecasting, performance management, and analysis. Each is distinct but complementary.

Planning

Planning is where FP&A begins. Its most essential output is the budget: a financial roadmap, typically built at the start of each fiscal year, that allocates resources to their highest and best use in pursuit of company goals.

A well-constructed budget does more than set revenue targets and expense limits. It reflects deliberate choices about where the business will invest, where it will pull back, and what tradeoffs it is willing to make to achieve its strategic priorities. A business may decide to invest more heavily in sales headcount, technology infrastructure, or new market entry. Each of those choices carries financial consequences. FP&A helps leadership understand those consequences before resources are committed.

For a deeper look at how budgeting works in practice, see Three Types of Business Budgets.

Forecasting

Forecasting is the function that keeps the business grounded in reality as the year unfolds. A budget is set once and does not change. Business conditions do.

A forecast incorporates actual results as they become available and refines the assumptions underlying the original plan, producing an updated picture of where the business is likely to land. FP&A teams typically update forecasts monthly or quarterly. At a minimum, a forecast covers the remainder of the current fiscal year. In many businesses, the forecast extends two to three years into the future.

That forward horizon is what makes forecasting a genuine management tool rather than a restatement of the plan. It helps leadership answer questions such as:

- Are we still on track to hit our revenue and profitability goals?

- Is cash flow tightening, and if so, what is driving it?

- Are gross margins improving or deteriorating, and why?

- Do current trends support the original plan, or does the business need to adjust course?

Without a regular forecast, leadership is often making decisions based on a plan that no longer reflects the business.

Performance Management

Performance management is how FP&A monitors progress against plan. It includes reporting, variance analysis, KPI tracking, and recurring financial reviews that help leadership understand whether the business is on track and why results are coming in the way they are.

Reporting is an output of performance management, not the goal. A good FP&A process does not simply show that revenue was below budget or expenses were above plan. It explains what happened, why it matters, whether it is likely to continue, and what leadership should consider doing next. That is the difference between seeing a number and understanding the business.

Analysis

Analysis is the thread that runs through planning, forecasting, and performance management alike. It answers the questions that raw data cannot:

- Why did gross margin decrease last quarter?

- Which product lines, services, customers, or locations are the most and least profitable?

- If headcount grows by 20 percent next year, what happens to the company’s cost structure?

- What happens to cash flow if sales slow, collections are delayed, or costs rise?

Analysis surfaces the patterns, relationships, and implications in financial data that inform decisions about hiring, pricing, investment, and growth. It is what transforms financial information into something leadership can act on.

Together, these four activities define what FP&A does. A business that plans without forecasting operates on assumptions that go unchallenged. A business that reports without analyzing knows what happened but not what to do about it.

FP&A vs. Accounting: Why the Difference Matters

Every growing business starts with accounting, and for good reason. Accurate books, tax compliance, and financial reporting are foundational requirements. Without them, nothing else in finance works.

But accounting and FP&A serve different purposes. Accounting answers the question: what happened? FP&A answers the questions that come next: why did it happen, what does it mean, and what should we do next?

| Aspect | Accounting | FP&A |

|---|---|---|

| Orientation | Primarily backward-looking | Primarily forward-looking |

| Core function | Records financial transactions | Interprets financial results |

| Primary outputs | Financial statements | Budgets, forecasts, analysis, decision support |

| Focus | Accuracy, compliance, and historical reporting | Planning, performance, risk, and future outcomes |

| Key questions | What happened? | Why did it happen, what does it mean, and what should we do next? |

Accounting records what has occurred: revenue recognized, expenses incurred, assets owned, liabilities owed. Its standards are defined by accuracy, completeness, and compliance. FP&A takes that historical record and asks what it means for the future, helping leaders understand what choices are available and how decisions may affect profitability, cash flow, growth, and enterprise value.

The two functions are complementary, not competing. FP&A depends on accurate accounting data to do its work well. But knowing what happened is not the same as knowing what to do next. As a business grows and financial complexity increases, leadership needs both. For a closer look at how these two functions relate, see Accounting vs. Finance.

Signs Your Business Needs FP&A Now

For many businesses, FP&A is not a function they set out to build. It becomes necessary as the organization outgrows what accounting alone can provide. The challenge is recognizing when that threshold has been crossed.

These are common signs that your business may need FP&A now.

Financial reports are available, but the story behind them is not clear.

You can see the numbers but struggle to explain what is driving performance. Revenue may be up but profitability may be flat. Expenses may be over budget, but it is not clear whether the issue is timing, volume, pricing, hiring, productivity, or something more structural. FP&A translates financial results into a management narrative leadership can use.

There is no regular forecasting process.

Actual results accumulate, but they are not used to update assumptions or refresh the financial outlook. Leadership is making forward-looking decisions based on a plan that no longer reflects current conditions. A regular forecast keeps the business grounded in reality and allows for course correction before problems become urgent.

Hiring, pricing, or investment decisions lack a financial framework.

Consequential decisions are being made on instinct or incomplete information rather than forward-looking analysis. Should the business hire ahead of growth or wait? Can it afford a new system, location, product line, or sales initiative? FP&A provides the analytical framework to evaluate options and quantify tradeoffs before resources are committed.

Profitability is unclear below the company level.

Revenue is coming in, but there is no clear picture of which products, services, customers, or lines of business are most and least profitable, or what can be done to improve the mix. Without that visibility, decisions about pricing, cost structure, and where to invest for growth are difficult to make with confidence.

Cash flow visibility is limited.

For businesses that have raised capital, including portfolio companies operating under PE or institutional ownership, understanding runway and cash burn rate is critical. Without a reliable forecast, these questions are difficult to answer with confidence, and by the time cash pressure builds, the window to act has often narrowed. FP&A gives leadership earlier visibility into potential constraints and the options available to address them.

The business is approaching a significant inflection point.

A capital raise, acquisition, major expansion, or potential exit requires a higher level of financial rigor. Standard accounting reports are not enough. These moments require forward-looking analysis, credible forecasts, scenario planning, and clear explanations of the financial drivers of the business.

Any one of these signs is worth taking seriously. Together, they indicate that the business has reached a stage where FP&A is no longer a nice-to-have. It is what makes the difference between reacting to financial outcomes and getting ahead of them.

How FP&A Evolves with Your Business

FP&A does not look the same at every stage of growth. Building the capability does not require starting with a full team. What matters is that the function exists in a form proportionate to the complexity and ambitions of the business, and that it continues to develop as those demands increase.

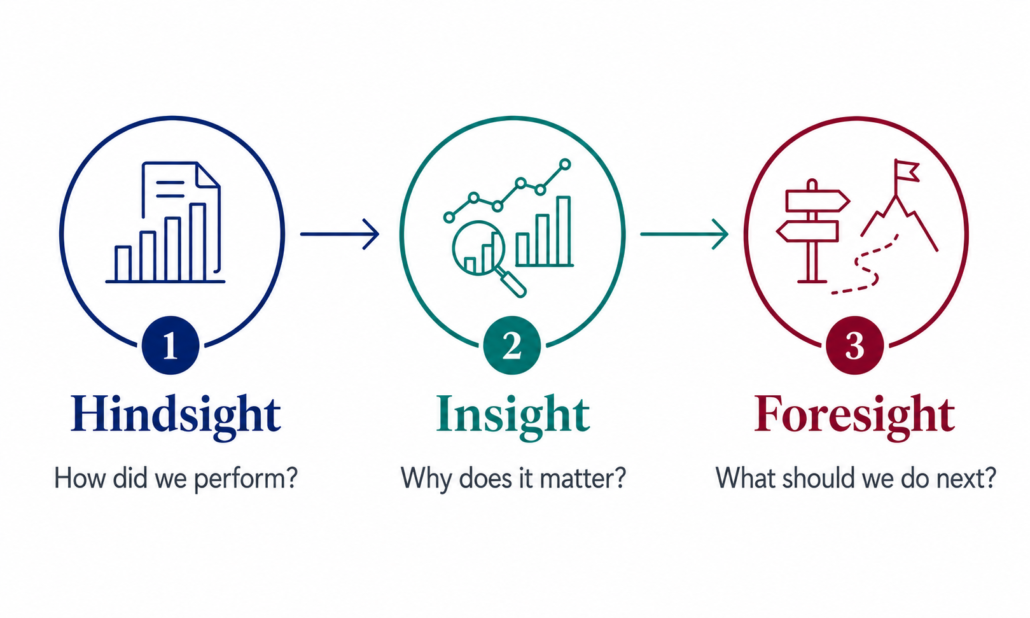

A useful way to think about FP&A maturity is the progression from hindsight to insight to foresight.

Stage 1: Hindsight

At the earliest stage, many businesses have no standalone FP&A function. Accounting staff handle some budgeting and reporting responsibilities alongside their core work. The finance function has not yet developed true FP&A capability: the budget exists as a fixed reference point, reporting is largely descriptive, and forward-looking analysis is limited. The business can see what happened but has limited ability to explain what it means or anticipate what comes next.

Stage 2: Insight

As complexity grows, the business needs a more deliberate FP&A capability. This is often the stage where a fractional FP&A engagement delivers significant value: bringing enterprise-level analytical capability to bear without the cost or overhead of a full-time hire. Forecasting becomes more regular, accurate, and rigorous. Reporting becomes more purposeful, delivering the right information to the right people at the right time rather than distributing a standard package. FP&A begins to shift from hindsight to insight, explaining not just what happened but why, and what it means for the decisions ahead.

For businesses ready to think about building a more formal function, see How to Build an FP&A Team.

Stage 3: Foresight

At the most developed stage, FP&A operates as a genuine strategic partner to leadership. Planning and forecasting are integrated across the business, scenario analysis is built into the regular management cadence, and finance is a trusted source of foresight for the CEO, board, and investors. This is where FP&A helps leadership evaluate not just what is likely to happen, but what could happen under different assumptions, and what decisions should be made now as a result.

For businesses that have raised institutional capital or are operating under PE ownership, FP&A expectations are typically more demanding from the outset. Investors and sponsors require regular, detailed reporting, rigorous forecast accuracy, and the analytical infrastructure to support portfolio-level decision-making.

Building that capability well requires clarity about what FP&A needs to deliver and how it fits within the broader finance organization.

Common Questions About FP&A

What does FP&A stand for?

FP&A stands for financial planning and analysis. It is the corporate finance function responsible for budgeting, forecasting, performance management, financial analysis, and decision support. In practical terms, FP&A helps leadership understand where the business is headed, what choices are available, and what decisions may be needed to improve performance, manage risk, and support growth.

How is FP&A different from accounting?

Accounting records what has happened: revenue, expenses, and the financial position of the business at a point in time. FP&A takes that historical record and asks what it means for the future. Accounting answers “what happened?” FP&A answers “why did it happen, what does it mean, and what should we do next?” The two functions are complementary. Businesses build accounting capability first and add FP&A as complexity and growth demands increase.

Does my business need a dedicated FP&A hire?

A dedicated FP&A hire is not always necessary right away. Many businesses benefit significantly from FP&A capability before they are ready to justify a full-time role. An outsourced FP&A engagement can provide enterprise-level planning, forecasting, and analytical support on a part-time or project basis, scaled to the needs and stage of the business. As the function matures and demand increases, building toward a dedicated role or team becomes a natural next step.

When is the right time to invest in FP&A?

The right time is earlier than most businesses act on it. The common trigger is a problem that has already become visible: a cash flow crunch, a missed forecast, a capital raise that exposed gaps in the financial infrastructure, or a board meeting where no one can clearly explain what is driving performance. The businesses that get the most value from FP&A invest in it before those moments arrive, using it to anticipate outcomes and identify risks before the business is forced into a reactive posture. If your business is growing, managing investor expectations, making significant resource decisions, or approaching a major inflection point, building FP&A capability before the need becomes urgent is the right call.

What is the difference between FP&A and a CFO?

A CFO is a senior leadership role with broad responsibility for the financial health of the business, including accounting, treasury, capital structure, investor relations, and strategic financial leadership. FP&A is a function within the Office of the CFO focused specifically on planning, forecasting, performance management, analysis, and decision support. In smaller businesses, a fractional CFO may perform both roles. As a business scales, the two often become distinct, with FP&A serving as the analytical engine that supports informed decision-making across the leadership team.

The Bottom Line

FP&A is the corporate finance function that transforms financial data into forward-looking insight. Through planning, forecasting, performance management, and analysis, it gives leadership the clarity to allocate resources, manage risk, and pursue growth with confidence.

Every business starts with accounting, and accounting remains essential. But as a business grows, knowing what happened is no longer sufficient. Leadership needs to understand why results are coming in the way they are, anticipate what comes next, and make informed decisions before the window to act has closed. Better visibility, stronger forecasts, more disciplined resource allocation, clearer tradeoffs in decision-making, and more confident board and investor communication: that is what FP&A makes possible.

Whether your business is navigating its first serious growth phase, preparing for a capital raise, managing investor expectations, or building toward an exit, FP&A is what separates reactive financial management from deliberate, forward-looking strategy.

If your business has outgrown basic financial reporting and needs better forecasting, visibility, or decision support, schedule a free introductory consultation with Momentum CFO.

{kind=link}